Not A Subscriber?

Join 10,000+ readers on building a life rooted in freedom, wealth, and meaning.

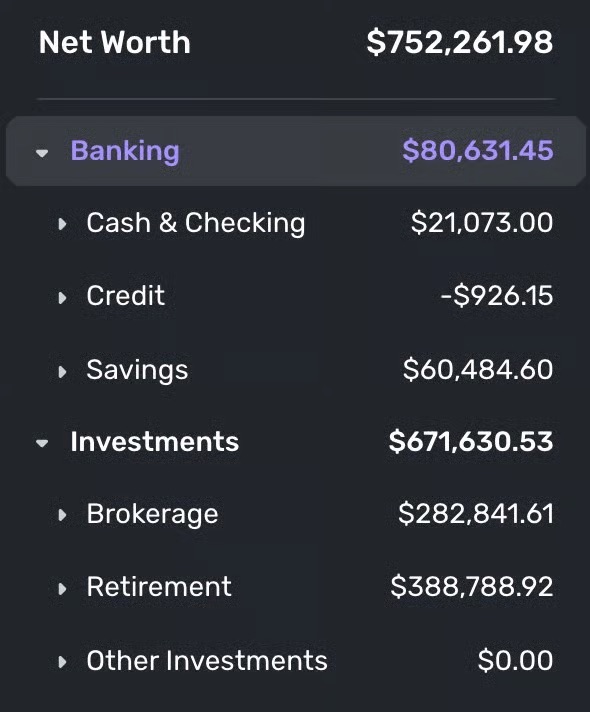

Coming Clean on My $750K Net Worth at 27

September 4, 2025 · Jim Tang

Trust fund, baby.

Just kidding. But before I dive into my journey to this number, I want to make a disclaimer.

I'm extremely transparent with money. It triggers some people.

But I accept that cost because I write for my 22 year old self.

The one who felt trapped in the hamster wheel that we call corporate. Convinced that this was his life for the next forty years.

In this newsletter, I want to talk about the concepts that got me out of that rut.

Because even though I wouldn't prescribe the path I took to everyone, I want to bridge the gap on how I developed my new beliefs.

Before I get into this story, this is some important background info:

-

My parents covered my tuition ($100k total across 4 years)

-

I graduated into the pandemic and lived at home for 1.5 years

-

My family lived paycheck to paycheck while I was a kid, but not in meaningful debt

Altogether, this puts me at around top 20% of privilege in America.

While we will go over wealth-building principles, this edition of Escape Velocity isn't meant to be a personal finance blog post.

This is a recounting of my 5.5 years of building wealth with the most essential lessons I've learned along the way.

Let's get into it.

The Trigger

One week into my new grad job at American Express, I was ready to quit.

I had a mid-level engineer teammate and he was essentially my micromanager.

I'd code up changes but it didn't matter if they were right or not. What mattered was that it was done his way.

If he wanted to change the approach, I rewrote the whole thing. If he wanted to hop on a call, I hopped on a call. I couldn't stand it.

But at 22 years old, I was bottom of the totem pole. Not to mention, I had zero leverage.

If I quit, I'd lose my health insurance. If I underperformed and got let go, I'd have no money.

If either of these happened, I'd look like a failure to my friends, my parents, and to the Chinese American community they lived in - to be unemployed would mean having our names dragged through the mud in gossip.

It was on those days that I regretted spending all my internship money living in NYC and on Chick Fil' A.

Every day that I had to hop on a call after hours, or to redo my code to fit arbitrary opinions, I had a recurring thought:

This is life? Forty more years… of this?

Desperation led me to desperate searches on Google:

"just started work want to retire."

At that point, I didn't care about feeling weak or undisciplined. I just wanted a way out without ruining my life.

That's when I came across FIRE.

Discovering FIRE (Financial Independence, Retire Early)

On a little corner of the internet, I came across a community.

People who weren't waiting to 65 to retire, but rather, as early as their 30's and 40's.

I was hooked.

The gist of FIRE is this: Invest enough money and you never have to work again.

This community railed against the normalized paycheck to paycheck until 65 lifestyle.

When I came across this, I instantly started fantasizing about hitting financial independence and being able to:

- Say "f*ck you" to my teammate and to any corporate politics.

- Quit my job and play video games to my heart's content.

So I got to work. I calculated that I wanted to be able to spend $80k/year in retirement. I plugged that number into calculators.

My tentative FIRE number was $2 million.

Then, it was time to execute.

There’s nuances to financial independence that I am not going into here. I’d recommend reading the r/financialindependence wiki for a primer if you’re interested.

The Timeline Behind My $750K

Here's the breakdown of how I actually built wealth:

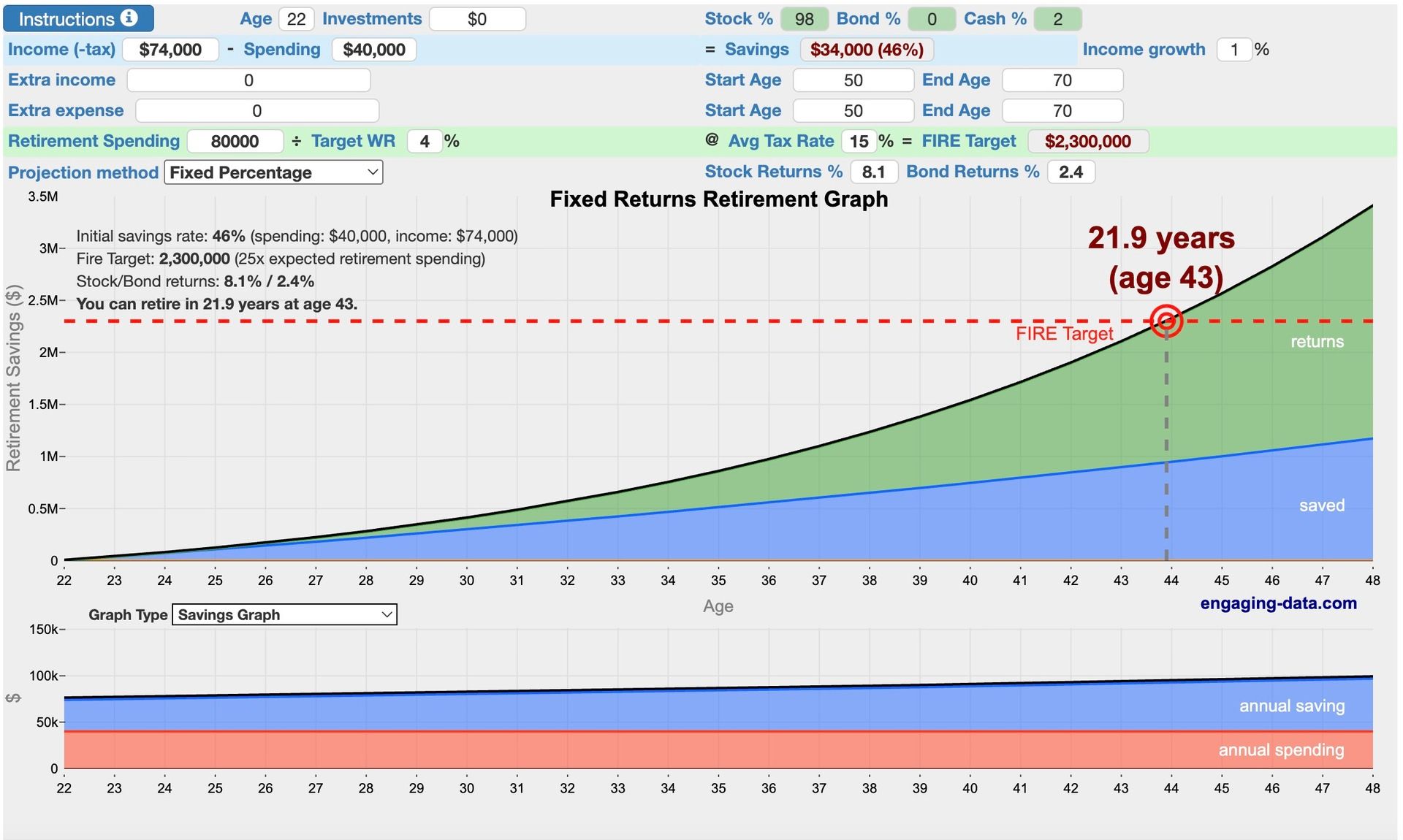

Ages 22-24 (American Express era):

- Total comp: $92.5k → $102k

- Expenses: ~$10k (living at home)

- Net worth: ~$140k

When I plugged in my FIRE number at my AmEx income, this was what I got:

Calculator: https://engaging-data.com/fire-calculator/

My actual expenses were around $10k from living at home like I mentioned, but I plugged $40k because I didn't want to live at home forever. At American Express, assuming no major salary jumps I would hit my number at 43 years old.

During this time, I started tracking my net worth, investing in my 401k, and putting my excess income into low-cost index funds (primarily VTSAX).

And when the opportunity arose to skyrocket my income during the tech boom, I took it.

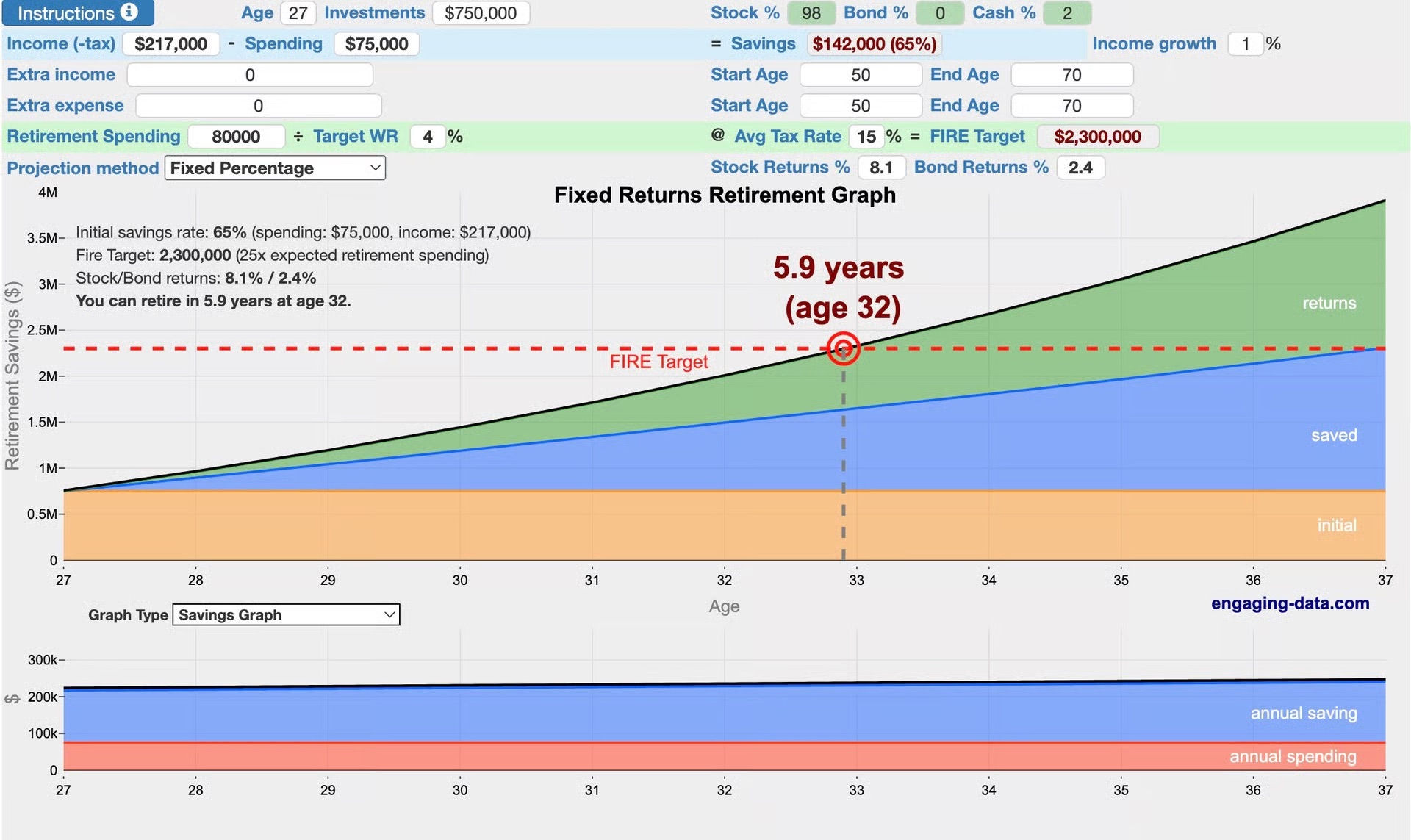

Ages 24-27 (Google era):

- Total comp: $226k → $350k

- Expenses: $40k → $70k (NYC w/ roomates → NYC solo)

- Final net worth: $750k

When I quit Google at 27 years old, I was on track to hit over $2 million at 32 years old (assuming no significant market crashes).

Calculator: https://engaging-data.com/fire-calculator/

A whole 11 years faster than if I stayed at American Express. That's not even accounting for promotions, annual raises, and the increased expenses I had taken on.

Earning power is your ultimate wealth accelerant. We'll talk about that in the next section.

Totals (2020–2025, ~5.5 years):

- Total earned: ≈ $1.2M gross → ~$800k net (take-home)

- Total expenses: ≈ $250k

- Total invested / saved: ≈ $550k

- Total company 401k matches: ≈ $40k

- Investment gains: ≈ $160k

These are rough estimates and we leave out a lot of the tax-deductible income wonkiness.

But it paints the picture of the power of investing, earning power, 401k matching, and reduced expenses.

The Three Stages of Building Wealth

I went through a lot of technical stuff in personal finance.

I think it’s unnecessary for most people.

These three stages will outline the highest leverage moves you can make on your financial journey.

Stage 1: Become Bulletproof

When you start being prudent with money, you make yourself impervious to bad situations - economic downturn, loss of a job, medical emergencies.

To save your time, I'm not going to into emergency funds, paying down debt, or budgeting spreadsheets. You can find this information anywhere online.

I’m isolating the single lever that helped me be financially bulletproof without being miserly:

Set a percentage-based spending limit based on your income.

Because regardless of how much money you earn, if you live a lavish lifestyle that spends all of it, you're not safe from disaster.

The rule that I'd recommend is to avoid spending more than 50% of your post-tax income.

This isn't always possible if you don't make as much money, so tailor accordingly.

I've found this principle to be best because complete elimination of lifestyle inflation and living ultra-frugal isn't most people’s vision of life progression.

As you increase your income, it only makes sense to invest in things that would better your health and buy back your time.

To become financially bulletproof, you have two tasks:

- Get out of debt (mortgages are an exception)

- Set a percentage-based spending limit and stick to it.

Stage 2: Building Wealth

Once you get past stage 1, you’ll have income to actually save and invest.

Stage 2 is when you start actually building wealth.

While personal finance heads will debate optimizations, there are three core actions which I recommend to literally everybody because they are objective truths:

Invest your money

If you want to see the power of investing and compound interest, look at the first calculator image above and notice how the green arrow goes asymptotic.

I was surprised to find out that a significant number of my high-earning friends hold all their money in savings. If you do this, your money will get eaten up by inflation and it won’t work for you.

Simplest method here is to invest in index funds. I "made" $160k over 5.5 years from parking my money primarily in index funds.

You’ll have to open a brokerage account to do this. I recommend Vanguard (VTSAX) or Fidelity (FZROX).

Keep savings in a high-yield savings account

Literally no reason not to be earning 3%+ interest on any savings you have sitting.

I personally use Apple Savings (currently 3.8% interest) for convenience.

It’s free money.

Max out your employer 401k match.

More free money. Maxing your 401k employer match is 99% risk free. Not only is it tax-advantaged which is already great, but even if you for whatever reason have to withdraw all the money early, you'll still come out ahead compared to never contributing at all.

For this, you’ll have to see company policy.

Also, make sure you invest this money once it’s in your 401k. A lot of people forget.

There are many more optimizations like Roth/Traditional IRA’s and HSA’s. Again, r/financialindependence wiki is a good place if you want to learn more.

Stage 3: Acceleration

Stage 3 is when you combine spending less, investing, and earning more. This is when things really pick up.

The trap that I fell for (and 90% of FIRE members fall for) is over-indexing on frugality. Spending hours optimizing my budget and overthinking the tax-advantages and investments.

I didn't confront the fact that your earning power is the single greatest lever to building wealth.

This can take the form of getting a higher paying job. For me, I doubled my compensation by spending 4 focused months of interview prep. This job hop cut my estimated time to FIRE by 11 whole years.

If your industry is hard-capped on income, you can look towards alternatives like starting a side hustle or business.

Avoid Getting Stuck

Here's what I realized after five years of reading endless FIRE forums and progressing through the three stages myself:

The average American never gets to stage 1. They get stuck in a job they hate living paycheck to paycheck. Spending money to make life just above tolerable.

Most people who discover FIRE make to stage 2 and then stagnate. They over-optimize on esoteric knowledge thinking it’s the only option available. They fail to see that they are stepping over dollar bills to pick up nickels (maximizing income).

A select few reach stage 3 and realize… they solved their money problems, but they procrastinated solving the fundamental problem of life.

The Hidden Stage

By 27, I had achieved what most FIRE enthusiasts dream of: $750k net worth, $350k job, on track to hit my $2M target in under 5 years.

Yet I was depressed. I had everything I'd worked for, but was unable to explain why I felt so empty. I tried to “fix” myself by getting fit and hanging out with friends regularly, but nothing worked.

I’d been optimizing for the wrong kind of freedom.

The concept of FIRE frames your mind to think in a form of living life “one day" rather than building a life you love ASAP.

That turning point, when you have acquired the ability to build such a life is what I call reaching Escape Velocity.

While I don't subscribe to FIRE in its entirety like I used to, I wanted to write this newsletter to give you the same awareness and principles that once helped me.

For me, financial security turned into a foundation for all the things I’m doing now.

Hopefully, this knowledge can help you in a similar way.

Next week, I'll be discussing what I’ve learned on the hidden stage which I now call Escape Velocity.

See you then,

Jim

P.S. For those building toward their escape - I've opened early access to Creator OS, the systems and strategies I used to grow an audience from 0 to 235k in 5 months.

To be upfront, building an audience is arduous, scary, and far from get rich quick. But… it’s also the highest leverage thing I’ve done. If freedom feels distant, building an audience can give you options.

If that interests you, feel free to check it out.